Benjamin Pollock, CFA, Head of Institutional Sales and Investor Relations

Benjamin.pollock@jasperam.com

+(86)0755-6182-6936

Bush Guo, Vice President, Institutional Sales and Investor Relations

Bush.guo@jasperam.com

+(86)0755-6686-7369

Systematic investors can do their very best to try to read Beijing’s tea leaves on policy and regulation, but at the end of the day exogenous shocks in the form of policy and regulatory intervention are part and parcel of systematic investing.

What makes China’s risk environment extremely challenging this year is the task of coming to a conclusion on whether or not the exogenous shocks observed mark the start of a reform regime shift to be formalized in the upcoming 19th Party Congress. The answer to this question is pivotal for systematic investors that utilize value strategies.

This month’s newsletter is dedicated to explaining our view on whether or not a reform regime shift has been ushered in with the exogenous policy shocks introduced so far in 2017.

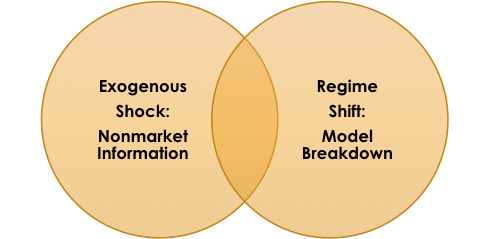

Exogenous Shock Risk

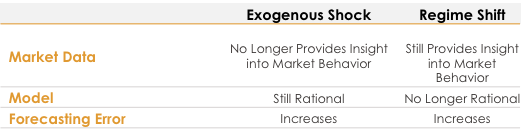

In China the most typical exogenous shock comes in the form of policy or regulatory intervention. Because systematic strategies rely on market data to produce forecasts, when nonmarket information heavily influences market behavior, systematic strategies often underperform. This is especially true because shocks often cause larger than normal moves that cannot be explained by models that use market data, but rather by external information.

Regime Shift Risk

Regime shift risk is best characterized by a breakdown in past relationships and market behavior. Systematic investing relies on past relationships and behavior to develop theories and build models to help forecast the future. If the relationships and stakeholder behavior upon which the models are based upon breakdown, forecasting error increases.

Differences and Similarities

Both risks mentioned above introduce the likelihood for greater forecasting error, but there are key differences between the two types of risk. Exogenous shock risk describes a scenario in which a rational model is being fed market data that no longer provides insight into market behavior. Regime shift risk describes a scenario in which a flawed model is being fed market data that still provides useful insight into market behavior.

Exogenous Shock Risk

Very little can be done to monitor or reduce exogenous shock risk ex ante, while discretionary overrides are the most reasonable ex poste option.

Regime Shift Risk

Continuous testing of the theories developed from past relationships and market behavior is the best approach to monitor and reduce regime shift risk.

Identifying Risk Overlap

If the source of risk which has caused greater forecasting error can be clearly identified, a definitive plan of action can be taken. However, if an exogenous shock is the catalyst for a regime shift, which in turn alters past relationships and market behavior, identifying the root cause of forecasting error becomes more difficult. In this case, nonmarket information and an irrational model are both potential sources of forecasting error.

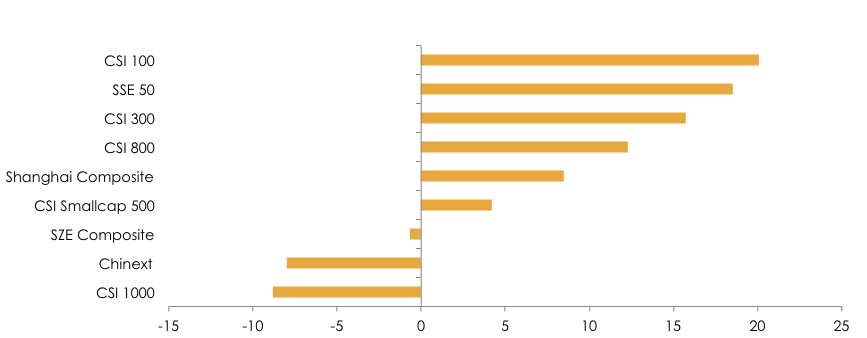

A large style performance disparity has been seen in China this year characterized by Blue Chip, Large Cap Value, and Cyclical shares significantly outperforming Small Cap, Mid Cap, and Growth peers. This outperformance can mainly be attributed to the exogenous policy and regulatory shocks that have taken place this year in the form of 1) advancing supply side reforms and industry consolidation measures, 2) stringent environmental protection crackdowns, 3) equity market regulations closing popular channels for secondary equity offerings, and 4) shareholder divestment regulations.

At first glance, these regulatory and policy shocks seem to be components of larger reform and development agenda. Therefore, it could be argued that the shocks in 2017 mark the start of a regime shift.

China Major Market Indices Return YTD (%)

Regime Shift Establishes New Reform Equilibrium

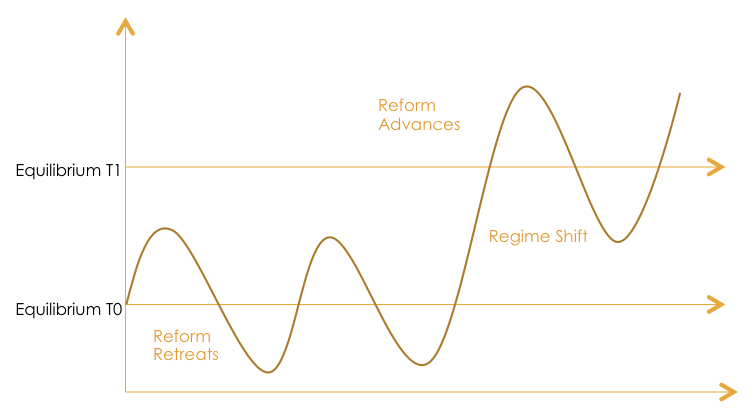

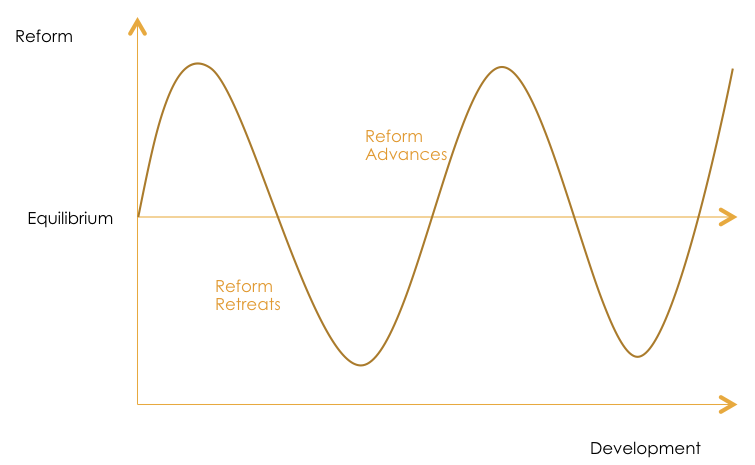

Astute followers of China’s political-economy recognize that policy and regulatory intervention often waxes and wanes around a stable equilibrium. The length of reform advancement or retrenchment in the reform cycle depends upon the growth outlook as well as political factors. From this perspective, it can be argued that the shocks that have occurred this year are unlikely to have significantly altered past relationships and market behavior.

To come to a more definite answer on this pivotal question, we must define China’s current and expected growth environment, political factors, and understand the mindset of China’s policymakers as it relates to growth and reform.

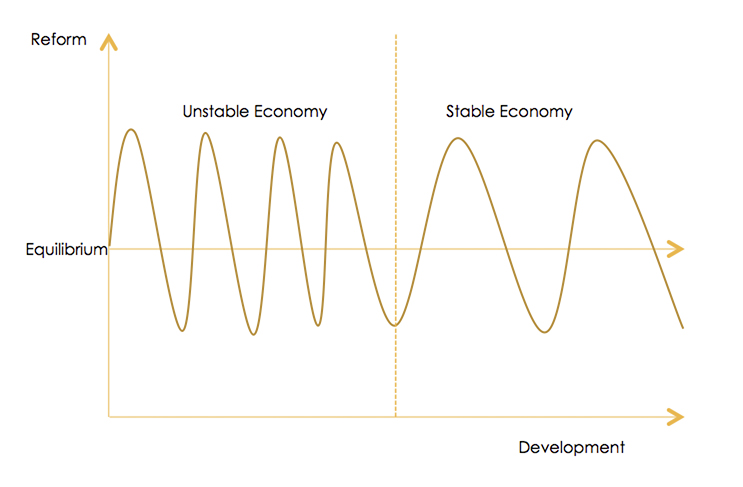

In general, the policymaker mindset is that reform has been the key driver behind China’s impressive 30+ year track record of fast-paced growth. Without reform, past development would have been difficult to achieve and future growth will be difficult to sustain. A condition of this mindset is that economic stability decides the strength of reform. If the economy is viewed as lacking stability, reform will recede in favor of stimulus. If the economy is viewed as being stable, stimulus will recede in favor of reform. Depending on the stability of the economy and political factors, policy makers might also decide to make adjustments to the frequency of the reform cycle. But, institutional memory of past success often prevents policy makers from shifting to a new reform equilibrium because the consequences of deviating from the current path are unknown.

Reform Waxes and Wanes Around a Steady Equilibrium

Frequency of Reform Cycle Adjusted Around Current Equilibrium

Based on this year’s accelerating growth, tighter monetary policy stance, and stable fiscal policy, it seems highly likely that policymakers are not greatly concerned about macroeconomic risks.

In other words, economic stability has opened the gate for reforms to advance in a similar way as in the past, i.e., a phase of advancing reform around the current reform equilibrium. The frequency of the reform cycle has perhaps been slightly adjusted to reflect better-than-expected macroeconomic conditions.

However, given the complexity of the Chinese economy, the institutional memory of policy makers, and the stakes on the line for the government whose legitimacy is closely tied to economic performance, it is very unlikely that we are observing the start of a regime shift towards a new equilibrium.

Therefore, we can conclude that the risk we are seeing this year is an exogenous shock risk, not a regime shift risk. The larger than normal moves for specific styles and shares supports this conclusion.

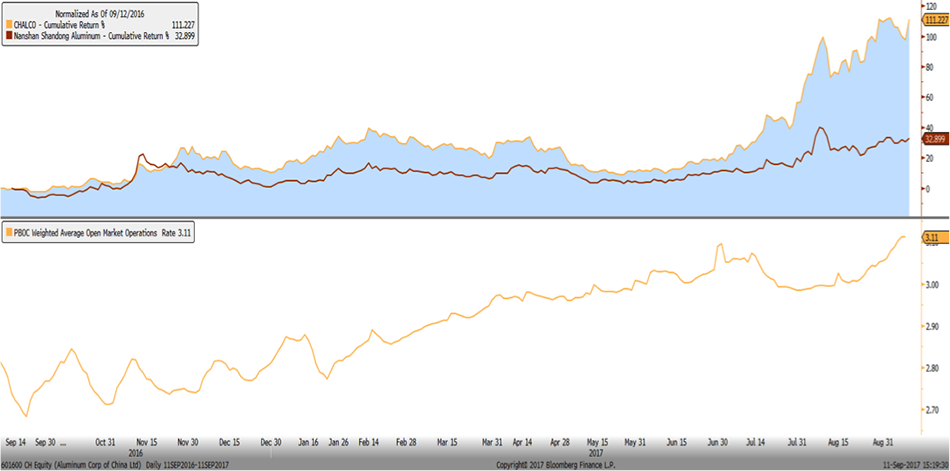

SOE CHALCO’s Cumulative Return Now Vastly Exceeds Non-SOE Peer Nanshan

Disclaimer: The information contained herein (the “Information”) is for illustration and discussion purposes only. It is not, and may not be relied on, as investment advice or as an offer to sell or a solicitation of an offer to buy any security, including any investment or any interest in the fund or funds referred to above (the “Fund”). The Information is not sufficient to form a basis for deciding to make any investment. It does not contain material information regarding the Fund, including specific information pertaining to an investment in the Fund and important risk disclosures. There can be no assurance and no representation, express or implied, is made that the Information is accurate. The Information is provided as of the date indicated, is not complete, is subject to change, and no obligation is undertaken to revise or update it.

Any offer or solicitation of an investment in the Fund may be made only by delivery of the Fund’s confidential offering documents. Prior to making any decision to invest in any fund, you are advised to obtain the fund’s offering documents, to perform your own independent review (in consultation with your own legal, tax, accounting and other advisors) of those materials, the fund, the fund manager as well as any performance data available to you.

An investment in the Fund is not suitable for all investors. Any offer or solicitation of an investment in the Fund may be made only to qualified investors in accordance with applicable law. In providing the Information, no action has been taken to qualify any potential investor, in any jurisdiction, including without limitation in the United States under the Securities Act of 1933 or the US Investment Company Act of 1940.

Past performance is not necessarily indicative of future results. There can be no assurance and no representation is made that the Fund will make any profit, and a total loss of principal may occur. The use of differing performance calculation methodologies may produce different results, and the Fund’s performance Information may not be comparable to the performance information provided by other funds or managers. Unless otherwise indicated herein, any performance or other financial Information included herein is unaudited, and the performance of data shown is net of fees (including without limitation management fees and performance fees) and expenses and presumes reinvestment of income.

All information contained herein is provided by the fund or manager and is solely the responsibility of the fund or manager.

深圳市福田区益田路5033号平安金融中心88层01单元

上海市浦东新区陆家嘴街道富城路99号 (震旦国际大楼)27层

香港中环德辅道中188号金龙中心17楼1701室